Table of Contents

01

Introduction to Private Equity Interviews in Australia

04

How to Prepare — A Practical Roadmap

02

What Private Equity Interviewers Are Actually Looking For

05

Real Cases and Lessons from the Field

03

Five Reasons Most Candidates Fail PE Interview in Australia

06

Conclusion

Introduction to Private Equity Interviews in Australia

Technical errors are rarely the reason candidates fail private equity interviews in Australia. Few candidates are rejected for PE jobs in Australia because they could not explain IRR or leveraged buyouts. They are rejected because they didn’t know how to apply that knowledge when tested, because their analysis was not specific to the case study, or because they appeared to be preparing for a finance job rather than a PE role. The question of why candidates fail PE interview in Australia is more complicated than it may seem – and knowing the answer is the first step to better preparation.

Australian private equity is a smaller, more connected market than those in the US and UK, and this has both positive and negative implications for job seekers. Getting a job in private equity Australia means not only showing you have the technical skills, but also an understanding of the industry, investment acumen, and the commercial skills learned on the job over the course of a deal cycle. The hiring firms are often small, with small deal teams that need candidates brought on to deals quickly.

This article is for finance professionals at the analyst/associate level who are seeking to understand what private equity interviewers are looking for, the five most common reasons candidates fail to convince, and how to develop a preparation strategy that addresses these five common failure points. Here, the insights are drawn from the experiences of successful and unsuccessful applicants – and the lessons are sufficiently common to be broader.

What Private Equity Interviewers Are Actually Looking For

The three dimensions of technical skills for PE interview in Australia

When it comes to technical PE interview in Australia skills, interviewers are looking across three dimensions, weighting them differently than expected. The first is basic finance skills: LBO models, DCF, EBITDA multiples, return on invested capital and debt structure. The second is analysis judgment: the ability to understand what drives the business and the quality of earnings, and to make a judgment on the investment’s attractiveness at the current price. The third – and most critical – is investment conviction: the ability to develop, articulate and defend a particular view of whether the business should be bought, at what price, and why.

• Candidates are well prepared on dimension one and not well prepared on dimension two, and those who exhibit strong analytical judgment and investment confidence, as well as competence.

• The questions that are asked in PE interview in Australia that test dimension three of the candidate – “tell me about a business you would invest in” or “what is your investment case for this business?” – are the questions that most candidates struggle with because their responses are generic rather than specific and justified.

What finance interview mistakes to avoid reveal about preparation quality

The investment question is the most important part of most PE interview in Australia. The interviewer who asks “why would you invest in this sector right now?” is not asking for a market description from a research report, but rather for a candidate who has actually developed a view, can explain the specific investment hypothesis, and can list the major risks that could falsify that view. Finance interview mistakes to avoid here include general comments about the sector, not knowing what would create value, and not knowing how the investment would go wrong.

• Private equity interviewers are looking for investment thinking, not rote memorisation; a candidate who explains that they don’t know but will age to uncertainty shows a more mature approach than one who claims to know everything and has no risks identified.

• Private equity interviews preparation questions and answers can’t be memorised; candidates who rote-learn answers to common questions tend to be caught out very quickly when the interviewer asks an unexpected question.

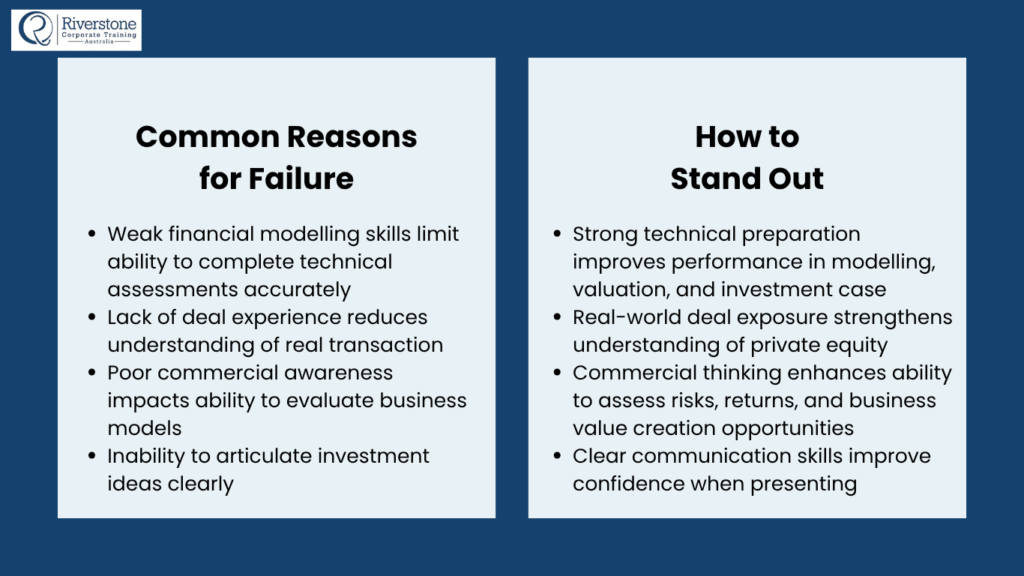

Five Reasons Most Candidates Fail PE Interview in Australia

The advice from industry practitioners who have been both interviewers and interviewees on preparing for private equity interviews consistently points to the same reasons for failure. Here are the top five most common and most avoidable.

| Failure Mode | How It Shows Up | Why Candidates Fail PE Interview in Australia | How to Address It |

| 1. Technical fluency without application speed | Candidate understands LBO mechanics but cannot build a basic model structure in the room or explain the returns impact of a 0.5x leverage increase without reaching for a calculator. | Finance interview mistakes to avoid: being technically correct but too slow; PE interviewers expect mechanics to be instant and automatic, freeing cognitive capacity for the investment judgment discussion | Practise building LBO model structures from scratch until they are automatic; time yourself; rehearse verbal returns analysis without a model |

| 2. Generic investment thesis with no specific conviction | When asked about an investment opportunity, the candidate describes a sector trend without identifying a specific business, a specific value creation angle, or a specific reason to act now rather than in 12 months | Common PE interview questions in Australia, like “walk me through an investment you would make”, expose generic preparation immediately; interviewers press for specifics and the generic answer collapses under the first follow-up | Prepare two or three specific investment ideas in detail: name the business, articulate the thesis, identify the value creation driver, size the return, and identify the key risks and how you would mitigate them |

| 3. No understanding of the fund’s own investment strategy | The candidate cannot accurately describe the fund’s sector focus, typical deal size, preferred entry and exit strategies, or recent portfolio activity — a fundamental signal of inadequate preparation | Preparing for private equity roles in Australia requires knowing the specific fund as well as the asset class; every fund has a differentiated strategy, and demonstrating that understanding signals genuine interest | Read every available piece of public information about the fund: website, portfolio companies, disclosed transactions, LinkedIn activity of the partners, any published commentary or interviews |

| 4. Inability to walk through a deal or model under pressure | When asked to walk through a transaction they have worked on, the candidate struggles to explain the key valuation decisions, the deal structure, or how the returns were modelled, because they were a junior participant who executed rather than analysed | M&A interview preparation guide: be able to own every deal on your CV; for each transaction, prepare a 3-minute structured walk-through covering the business, the thesis, the structure, the returns model, and what you learned | Prepare a structured 3-minute walk-through for every deal on your CV; anticipate every follow-up question and prepare specific answers; do not include deals you cannot fully explain |

| 5. Weak commercial awareness and market knowledge | The candidate cannot discuss current market conditions affecting PE deal activity, the impact of interest rate changes on LBO returns, or the sectors that are attracting or avoiding capital in the current cycle | Breaking into private equity in Australia requires demonstrating that you think about markets continuously, not just when preparing for interviews | Read the AFR, deal databases, and sector publications consistently; develop a view on the current deal environment before every interview; be able to articulate why the macro environment is favourable or challenging for PE returns right now. |

Failure moan de 2 – unconvincing investment thesis with no conviction – is the most common one that determines whether it sees candidates advance or fail, as it is the question that most clearly tests whether the candidate has been thinking like an investor or studying for an exam. Private equity interviews preparation tips that exclusively focus on the specific mechanics without developing investment thinking skills result in candidates who pass the initial screening interview but flunk the investment discussion. The investment thesis question is not a test of what you know; it is a test of what you think – and thinking is developed through practice, not rote learning.

How to Prepare — A Practical Roadmap

A structured private equity interview preparation tips programme

The passing to pass private equity interviews is a comprehensive prep tips programme. The roadmap below outlines how successful candidates spend the three- to six-month period before a targeted private equity interview preparation process.

| Phase 1(Months 1–2) | Phase 2(Months 2–3) | Phase 3(Months 3–4) | Phase 4(Month 4+) |

| Technical Foundation | Investment Thinking | Market & Fund Research | Practice Under Pressure |

| Build and time LBO models from scratch without templates; practise verbal returns analysis; review EBITDA multiples by sector; refresh DCF, debt structuring, and working capital mechanics until they are automatic | Develop two or three specific investment theses on real businesses; research each in depth: financial performance, competitive position, value creation angle, return model, key risks; practise presenting them out loud | Build a current view of the PE deal environment in Australia; research target funds deeply; prepare deal walk-throughs for every transaction on your CV; identify the fund’s differentiated strategy and recent portfolio activity | Run mock interviews with practitioners who will ask follow-up questions rather than accept rehearsed answers; practise defending your investment thesis under challenge; debrief every mock session and address the gaps |

Real cases: what separates the candidates who get offers

One corporate finance analyst, who wanted to switch to mid-market PE in Australia, spent four months preparing with a similar roadmap. The most impressive investment during interviews was not his ability to build an LBO model quickly (which he could do, but not super-fast), but his preparation of a particular investment thesis for healthcare roll-up services. He had mapped a sector with five similar roll-up platforms in nearby geographies; he modelled the acquisition of one particular platform with conservative synergy assurance, and had clear responses to all the obvious risks: the regulatory risk, the integration risk, and the risk that the roll-up thesis was flawed. He had gone even further in anticipating the downside. The deal was with the fund that had recently transacted in its portfolio in the health services sector. The fit between the thesis and the fund was prearranged through research.

A second interviewee with superior academic qualifications and the same level of experience failed the final round of the interview process. Her technical competence was top-notch. When she was asked to explain her most sophisticated deal, she detailed her involvement with a level of granularity that showed she had implemented parts of the deal without owning the investment or the structure. The interviewer’s subsequent questions – “why was the entry multiple appropriate for the risk profile?” and “how would the returns change if you delayed the exit for a year?” – revealed her lack of ownership of the deal beyond her experience as a participant. M&A interview preparation guide: Rule of thumb for every deal you have worked on: you have to own it.

Conclusion

The problem with Australian candidates failing PE interview in Australia is seldom a lack of technical competence. It is almost always a question of insufficient application: the inability to bring technical skills to the table in the form of investment judgment, the lack of a specific investment hypothesis to defend, or the lack of demonstration of understanding of the fund’s strategy and how the candidate will fit into it. Private equity interviews preparation tips that focus on all three areas – technical, analytical and commercial – result in well-prepared candidates, rather than technically proficient ones.

For candidates interviewing for private equity roles in Australia: know as much about the fund as you know about the industry – the ability to demonstrate that you understand the fund’s strategy, the fund’s portfolio, and why you are a fit for their strategy is the key to getting the job, not just getting feedback.

For private equity interviews in Australia, technical skills must be automatic, not deliberate; the time you save by not having to think about the mechanics is the time you spend demonstrating the investment judgment that sets the candidates apart.

To succeed in private equity Australia, a candidate must have a specific investment thesis, prepared to the point that it would stand up to a room of cynical practitioners; broad narratives about a sector do not pass the first question.

Private equity interviews typically include technical finance questions, investment case studies, LBO modelling exercises, valuation analysis, accounting concepts, and behavioural questions. Candidates are often expected to demonstrate strong analytical thinking, commercial awareness, and an understanding of how private equity firms evaluate investment opportunities.

Financial modelling skills are essential because private equity professionals rely on financial models to assess acquisition opportunities, forecast business performance, evaluate returns, and analyse investment risks. Interviewers frequently test a candidate’s ability to build or interpret valuation and leveraged buyout (LBO) models as part of the selection process.

Candidates should practise analysing businesses, developing investment theses, conducting valuation assessments, and identifying key risks and value creation opportunities. Reviewing real transactions, building financial models, and understanding industry dynamics can help candidates approach case studies with greater confidence and structure.

In addition to technical competence, interviewers look for commercial judgement, problem-solving ability, attention to detail, communication skills, and the ability to think critically under pressure. Candidates who can clearly explain their investment rationale and defend their assumptions often stand out during the interview process.

Candidates can improve their prospects by strengthening their understanding of valuation, LBO modelling, accounting, mergers and acquisitions, and investment analysis. Staying informed about recent transactions, practising interview questions, and developing a structured approach to investment evaluation can help demonstrate the skills private equity firms value most.