Table of Contents

01

Introduction to Build a DCF Model from Scratch

04

A Step-by-Step Framework for Building DCF Capability

02

Why Building a DCF from Scratch Is Harder Than It Looks

05

Real Cases and Lessons from the Field

03

Five Common DCF Mistakes That Undermine Valuation Quality

06

Conclusion

Introduction to Build a DCF Model from Scratch

How to Build a DCF Model from Scratch

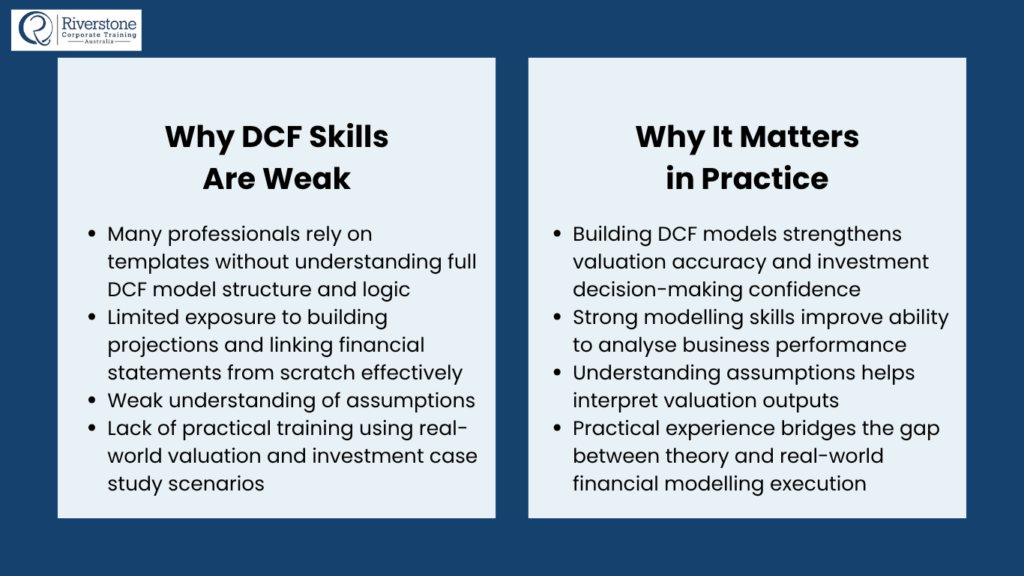

Building a DCF model from scratch is one such capability that most financial professionals assume they have, but in practice, few actually do. Present a room full of finance analysts with the question of whether they could create a discounted cash flow model, and nearly everyone in the room raises their hand. Ask them to do it on a live set of financial statements, no template, no pre-provided answer to the WACC, and no textbook answer to compare it to,o and you have a much thinner room. In practice, DCF modelling challenges are not the main technical challenge: the majority of professionals are familiar with the formula. The issues lie in the judgment calls that surround the formula, the normalisation work that precedes it, and the capability to defend the output to a client, an investment committee, or a similar party on the other side of the negotiation.

Why build DCF model from scratch is a difficult skill to learn is a question worth looking directly at, because the difference between knowing how to build a DCF model from scratch and having the ability to how to build a DCF model from scratch, nothing more than a set of accounts is even greater than most training programmes acknowledge. It is the distinction between being able to see the reasoning behind compound interest and being able to price a complex financial instrument: the concept is accessible, but the professional application requires a combination of technical fluency, data judgment, and contextualisation of a complex financial instrument that only develops through a process of deliberate practice on real material.

The article is targeted at finance professionals who wish to evaluate and develop their practical DCF modelling skills truthfully, and at professionals who design or commission valuation training who want to understand why standard approaches often fail to develop the skills they are meant to develop. The skill gap that has the most significant consequences within the valuation practitioner’s toolkit is the gap between theoretical knowledge and real-world DCF applications.

Why Building a DCF from Scratch Is Harder Than It Looks

The three layers of DCF modelling challenges

DCF modelling challenges lie in three layers, which most training discusses disproportionately. The former is mechanical: the model’s structure, formula logic, relationships among the three financial statements, and the derivation of free cash flow. The level of most finance professionals is sufficiently high. The second is judgmental: to choose the right period of projection, to justify the terminal growth rate, to choose the discount rate that reflects the specific risk the business presents, and to interpret what the model’s output actually says about value. It is in this layer that the actual abilities of most professionals are put to the test. The third is forensic: beginning with a set of actual financial statements, and determining what must be normalised, restated, or clarified before any projection is constructed. This is virtually a layer that is not covered in regular training.

• Where the most significant gaps in financial modelling skills lie is in the forensic layer – working between raw, imperfect financial data and a clean, analysis-ready base.

• The only way to be professionally competent in the modelling of the DCF is to ensure that all three layers are fluent: the mechanical layer cannot be fluent in isolation from the other two layers: the judgment layer and the forensics layer.

The discounted cash flow tutorial trap: why learning from examples doesn’t transfer

A discounted cash flow tutorial that takes you through a completed model develops familiarity and not ability. The learner who has just viewed five tutorial walkthroughs will not only understand the logic of a DCF but will also have practised generalising a specific DCF from nothing but a few pieces of information. He/she will not have practised making the judgments that the tutorial presenter has already made, or managing the ambiguity of real financial data that does not fit the model structure assumed. Step-by-step observation enables us to learn valuation models, which is only a starting point. The ability is built up through building, not through consumption.

• All the judgment calls made by the tutorial presenter on behalf of the learner are themselves judgment calls that the learner does not practise; the judgment call that builds ten models in a row is a judgment call that the learner does not practise.

• Data issues, structural issues, and assumption issues that always arise in the real-world DCF applications, in other words, are an unavoidable part of real-world DCF readiness.

Five Common DCF Mistakes That Undermine Valuation Quality

The five main areas in which common DCF mistakes in practice occur are as follows. Awareness of the areas of error concentration is a precondition for the targeted capability enhancement.

| Mistake | How It Manifests | Practical DCF Modelling Skills Implication | How to Avoid It |

| 1. Projecting from reported earnings rather than normalised cash flows | The DCF is built on reported EBIT or EBITDA without removing owner add-backs, one-off items, or non-arm’s-length transactions; the projection period perpetuates distortions from the historical period | Common DCF mistakes that start from unadjusted financials produce a model that appears technically correct, but values a business that does not actually exist; the error is invisible within the model | Always reconstruct normalised EBIT from the ground up before beginning any projection; every line item in the historical P&L must be assessed for sustainability before it is used as a projection base |

| 2. Using the firm’s cost of capital for a project with a different risk profile | WACC is sourced from the firm’s existing capital structure without adjustment for the specific risk of the business or project being valued | DCF modelling challenges from WACC misapplication are among the most consequential: a 200bps error in the discount rate applied to a five-year projection produces a material and directionally wrong valuation | Source the discount rate from comparable pure-play companies in the target’s risk category, not from the acquirer’s own WACC; document the specific comparables and adjustments used |

| 3. Terminal value that dominates the analysis without scrutiny | The terminal value represents 70–85% of the total DCF value in most private company valuations, but is built on a terminal growth rate selected without rigorous justification | Building a DCF model from scratch requires that the terminal value assumptions are as rigorously justified as the projection period assumptions; a terminal growth rate of 3% requires a specific argument, not a generic convention | Test the implied terminal EBITDA multiple against market comparables; if the terminal value implies a multiple that is not achievable in the market, the terminal growth rate needs to be revised |

| 4. Circular references in the debt and interest schedule | Interest expense is modelled as a percentage of opening debt, but debt changes with free cash flow generation; the model is internally inconsistent and cannot be relied upon for sensitivity analysis | Financial modelling skill gaps in debt scheduling are common and often undetected; the model appears to work, but produces different results in different scenarios because the debt-interest relationship is not correctly modelled | Build a separate debt schedule that tracks opening balance, drawdowns, repayments, and closing balance; calculate interest on the average of opening and closing balance; test the model’s sensitivity to free cash flow changes and verify the debt schedule responds correctly |

| 5. No sensitivity analysis on the most influential assumptions | The DCF produces a single point estimate that is presented as the valuation without any analysis of how sensitive the conclusion is to the key assumptions | Mastering DCF modelling requires that sensitivity analysis is built in from the outset, not added after the base case is complete; the range produced by the sensitivity analysis is typically more informative than the base case point estimate | Build a sensitivity table showing the implied valuation at five WACC levels and five terminal growth rates; the intersection of these two variables accounts for the vast majority of valuation variance in a typical DCF. |

The most commonly occurring mistake, which yields the most misleading results, is mistake 3: the terminal value that dominates without question. When the terminal value is 80 per cent of the total DCF value, it is modelled on a terminal growth rate chosen by convention rather than on a specific analytic justification. The step-by-step construction of learning valuation models must explicitly include the terminal value construction and a sanity check against market comparables; the terminal value is neither a residual calculation completed after the real work is done nor the most consequential number in the model.

A Step-by-Step Framework for Building DCF Capability

From a discounted cash flow tutorial consumer to a model builder

The development pathway that takes the professional through all three levels of DCF capability: mechanical, judgmental and forensic- is required in the real-world application of DCF. The four-stage model below illustrates how practitioners who become truly skilled at constructing the DCF model in their original design structure their work.

| Phase 1 | Phase 2 | Phase 3 | Phase 4 |

| Mechanical Fluency | Forensic Foundation | Judgment Development | Pressure Testing |

| Build the three-statement model from scratch without a template: income statement, balance sheet, and cash flow statement linking correctly; derive free cash flow to the firm; apply discount rate and terminal value mechanics; complete without referencing a tutorial mid-build | Take a real set of unformatted management accounts; identify every normalisation adjustment required before building any projection; document each adjustment with a specific rationale; compare your normalised EBIT with a practitioner’s independent reconstruction | Build the same DCF for five different businesses across different sectors; for each, justify the terminal growth rate with a specific sector argument, source the WACC from comparable pure-play companies, and document why you weighted the three methodologies the way you did | Present your completed DCF to a practitioner and invite challenge on every assumption; defend each judgment call without looking at the model; rebuild the model with the revised assumptions that emerged from the challenge; note what changed and why |

Real cases: the gap between knowing and doing

To evaluate the DCF capabilities of eight analysts at an advisory firm, the corporate finance team asked each analyst to build a DCF on his/her own, without a template or prior briefing. Eight of them had undergone a DCF-oriented training in the last 18 months. The results were shocking: four produced models with structural errors in the materials that would have produced unreliable sensitivity analyses, and two produced models with structural errors. Still, they applied a WACC clearly derived from the acquirer’s cost of capital, rather than the target’s risk profile. This produced a correct model and was well justified, but again had not completed any normalisation of the historical accounts, projecting off reported earnings without adjustment. The analyst who made the right, normalised, well-justified model was the only analyst who, in the course of developing the model, practised building a DCF model from scratch on real accounts. The remaining seven had been taught DCF methodology using tutorials and had done training exercises using pre-cleaned data.

The second scenario is that of a financial analyst who was requested to prepare a preliminary DCF for a prospective acquisition in her company. She created a model with a terminal value of about 87 per cent of total enterprise value and a terminal growth rate of 3 per cent, which she termed normal. After a senior colleague reviewed the model, he asked her to double-check the terminal value by computing the implied EBITDA multiple that it generated. The implied multiple was 18.4x – about twice as much as the sector had actually transacted over the last 5 years of known transactions. The terminal growth rate had to be reduced to about 1.8 per cent to generate a terminal value in line with the market comparables. The updated DCF generated a valuation range about 22 per cent lower than the original one. Arithmetic errors are not common DCF errors in terminal value construction; common DCF mistakes are errors in judgment that generate models that seem internally consistent but externally implausible.

Conclusion

The ability to develop a DCF model by hand distinguishes finance professionals who can develop credible, defensible valuations from those who can fill in a template. Practical DCF modelling skills of the level required of professional practice span three layers, mechanical, judgmental, and forensic; and are developed, rather than observed, through construction. The judgment and forensic layers of DCF modelling pose the most consequential challenges, with assumptions that drive the entire output being made and errors that most frequently result in misleading valuations.

• The best way to learn DCF modelling is to create models using raw, imperfect financial data many times, not to learn how to use the book or to practise on teaching datasets; judgment and forensic skills can only be developed through real practice.

• Common DCF mistakes are nearly always in the formula logic: in the normalisation decisions, in the derivation of the discount rate, and in the justification of the terminal value. The mechanical layer is the least difficult to develop and the least significant for output quality.

• For practitioners: Before making any DCF available to a client or a committee, present every DCF you construct to a critical peer, specifically inviting the critical peer to challenge the normalisation choices, the derivation of the WACC, and the justification of the terminal growth rate in particular.

A Discounted Cash Flow (DCF) model is a financial valuation method used to estimate the intrinsic value of a business based on its expected future cash flows. By forecasting future cash generation and discounting those cash flows back to their present value, finance professionals can assess whether a company, project, or investment is fairly valued.

Building a DCF model typically involves forecasting revenue and operating performance, calculating free cash flow, estimating a terminal value, determining an appropriate discount rate such as the Weighted Average Cost of Capital (WACC), and discounting future cash flows to arrive at an enterprise value.

A DCF model relies on accurate financial forecasts and a solid understanding of how the income statement, balance sheet, and cash flow statement interact. Strong financial modelling skills help ensure assumptions are realistic, calculations are accurate, and valuation conclusions are supported by sound analysis.

Common mistakes include using unrealistic growth assumptions, applying an inappropriate discount rate, overlooking capital expenditure requirements, and failing to perform sensitivity analysis. Because DCF valuations are highly sensitive to assumptions, even small errors can significantly affect the final valuation outcome.

Learning DCF modelling is valuable for finance professionals, investment analysts, corporate finance teams, business owners, students, and anyone involved in investment evaluation or business valuation. The ability to build a DCF model from scratch helps develop a deeper understanding of valuation principles and financial decision-making.