Table of Contents

01

Introduction

04

How to Close the Gap: A Practical Pathway

02

What University Finance Teaches and What It Doesn’t

05

Real Cases and Lessons from the Field

03

Five Valuation Skills That University Finance Doesn’t Develop

06

Conclusion

Introduction

The Gap Between University Finance and Real Valuation Work in Australia

A deep-rooted structural imbalance in the Australian finance labour market is the difference between the university and the real world. Graduates have learned to enter the first jobs in valuation work in Australia with a solid grasp of discounted cash flow methodology, an understanding of comparable company analysis, and a conceptual understanding of how the markets price risk. What they usually don’t have is the ability to use any of these frameworks to apply them to a set of real financial statements with all the imperfections, inconsistencies, and judgment calls that real financial data entails. The failure to address a finance education gap in Australia is not because universities are failing to provide students with the right concepts; it’s because they should be developing the right translation skill: using conceptual understanding in a professional context.

Theories and practices of financial skills in the valuation issue differ at a definite, known stage, known as the normalisation of financial statements. The clean, pre-formatted financial data needed for valuation work in Australia is available from the University’s curriculum. Once all the basic management accounts are in place, real valuation work in Australia begins with the financial statements, including owner add-backs, related-party transactions performed at non-market rates, one-off items that affect earnings trends, and capital expenditures inconsistently classified. The analyst who is unable to perform the normalisation exercise has not started the valuation work in Australia discussed in detail in the curriculum.

This article is for finance graduates looking to see what they do not know yet need to know and how to fill those gaps; for advisors looking to understand the finance graduate skill mismatch they face when onboarding new analysts; and for those creating practical finance development programmes who want to develop those specific skills that practical finance learning in Australia requires.

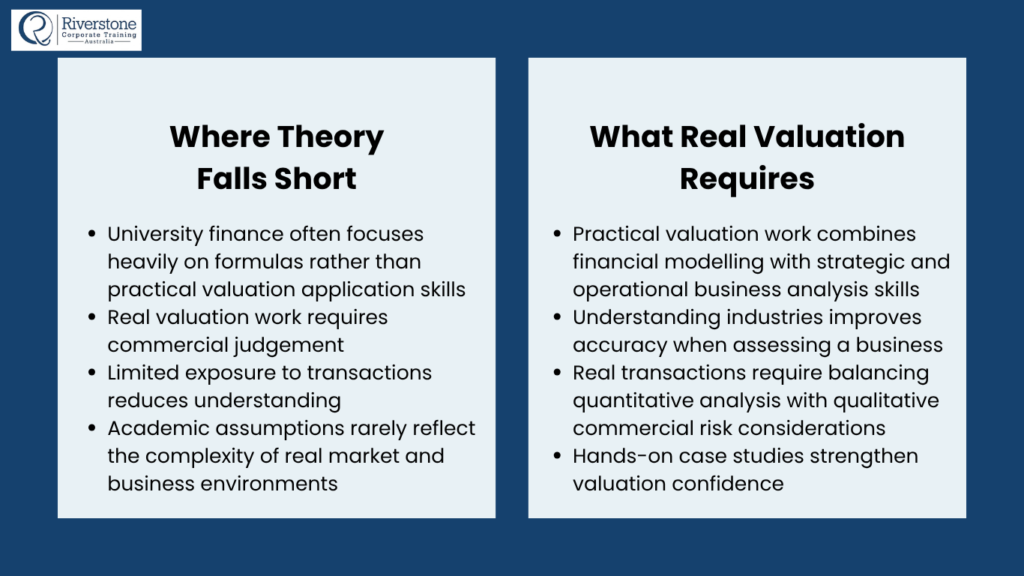

What University Finance Teaches and What It Doesn’t

The genuine strengths of formal finance education in academic vs industry finance

Academic vs. industry finance is sometimes framed as the idea that formal education brings nothing of value – the argument here is not that! The conceptual logic of time value is the first and most important foundation of university finance education, while the theoretical underpinnings of risk-return relationships, discounted cash flow analysis, and the relationship between valuation work in Australia methods and business finance value assumptions are the others. These foundations can’t be replaced with work experience, because they are the analytical structure that experienced practitioners continue to use even when the application is nothing like a textbook.

• The concepts taught in universities – WACC, Terminal value, Comparable multiples, Merger consequences, etc. – are useful; it is just the translation of these concepts into professional application that is missing.

• Bridging the finance education gap does not imply disregarding theoretical education; it means providing applied skills that the theoretical part of the curriculum does not provide and that are necessary for real valuation work in Australia from the first week of professional work.

Where real-world valuation skills needed diverge from academic preparation

There are three key ways that real-world valuation skills in practice differ from those taught in school. First, the data: when the university is exercising, it is using ready-made, complete financial statements; if real valuation work in Australia is to be done, the data must first be interrogated, normalised, and reconstructed before any analysis can be carried out. Second, the judgment: university exercises not only have correct answers, but real valuation work in Australia is also judgmental and reasonable practitioners will differ in their views on how to answer an ambiguous question, and forming and defending a position on an ambiguous question is not a skill developed by solving exercises with a marking key. Third, the communication – university assessments value technical accuracy, professional valuation work in Australia, and work that connects the analysis to the client’s real professional answer.

Five Valuation Skills That University Finance Doesn’t Develop

The finance skills gap when people are ready for work centres on a few core skills that the professional world demands and that are systematically missing from the University curriculum. Each is one type of translation mismatch between what is taught and the requirements of the first profession of valuation work in Australia.

| Skill Gap | How It Appears in Professional Practice | Finance Graduate Skill Mismatch Consequence | How to Close It |

| 1. Financial statement normalisation | Graduates can analyse a formatted financial statement; they cannot identify and adjust for owner remuneration above market rate, personal expenses in the P&L, related-party lease arrangements at non-market terms, or genuinely one-off items that distort the sustainable earnings base. | Valuation training shortcomings: graduates who cannot normalise financial statements cannot begin the valuation analysis that the curriculum covered in detail; they are applying a sophisticated methodology to an unrepresentative earnings base | Practise normalisation on at least five sets of real management accounts before entering a professional role; for each, identify every line item that requires a judgment about whether it reflects the sustainable, transferable earnings of the business finance |

| 2. Working backward from the market to the assumption | University DCF exercises provide the discount rate as an input; professional valuation work in Australia requires deriving the discount rate from market comparables and defending the choice; similarly, terminal growth rates are selected with specific sector arguments, not with a generic convention | Theory vs practical finance skills: the analyst who cannot justify the WACC from observable market data, or defend a terminal growth rate with a specific sector argument, is applying a sophisticated framework to unjustified inputs | Source WACC inputs independently for three different sectors using market comparables; compare the sector average to the firm-specific adjustment required for size, leverage, and country risk; practise articulating the justification for each choice out loud to a practitioner who will challenge it |

| 3. Selecting and adjusting comparable transactions | University comparable company analysis exercises provide a pre-selected peer set; professional work requires identifying which transactions or companies are genuinely comparable, understanding why each differs from the subject, and making specific adjustments for those differences | Finance education gap Australia: graduates who use a pre-provided comparable set without understanding comparability criteria cannot defend their multiple selections or explain why their range is appropriate for the specific business finance | Independently source comparable transactions for two businesses using disclosed deal databases; for each comparable, document the structural differences (control premium, deal structure, synergies) and the specific adjustment required; practise explaining why the adjusted range is more appropriate than the unadjusted one |

| 4. Forming and defending a valuation conclusion under challenge | University assessments produce a number; professional valuation work in Australia requires presenting a range, explaining the key assumptions, and defending the conclusion against active challenge from a client, an investment committee, or a counterparty | Academic vs industry finance: the analyst who can produce a DCF output but cannot explain why the assumptions are appropriate, or revise them credibly when challenged, has not yet developed professional valuation work capability | Present every valuation you complete to a practitioner who will actively challenge the key assumptions; practise explaining the assumptions without referring to the model; identify the specific points where your defence collapses and rebuild those positions before the next presentation |

| 5. Connecting valuation output to a commercial recommendation | University assessments reward the accuracy of the valuation calculation; professional valuation work rewards the connection between the valuation and a specific commercial action the client should take | Real-world valuation skills needed: the client does not pay for a number; they pay for a recommendation; the analyst who presents a valuation range without explaining what it means for the decision has completed the technical work but not the professional work | Complete every valuation work analysis with a written one-paragraph recommendation: what does this valuation work range imply for the specific decision the client is facing? What should they do, and at what price or under what conditions? Get feedback specifically on whether the recommendation is commercially actionable. |

Financial statement normalisation is the most basic gap, as it is the prerequisite for all other valuation skills. A sophisticated DCF model based on an unnormalised earnings base is built on an inaccurate foundation, and the imprecision of the inputs completely undermines the precision of the analytical model. The most important skill investment a graduate can make when entering a professional valuation work in Australia role is practical finance learning in Australia that focuses on normalisation in practice, using real management accounts with real imperfections. There is no substitute for this basic skill, even with additional methodological study.

How to Close the Gap: A Practical Pathway

A structured approach to bridging the finance education gap

Structured development programmes are needed to bridge an education gap in valuation, directly addressing the five gaps mentioned above and focusing on real financial data and real judgement decisions, not on pre-formulated exercises. The four-step process outlined below gives a glimpse of the progression of graduates who make the quickest strides to becoming productive valuation professionals.

| Phase 1 | Phase 2 | Phase 3 | Phase 4 |

| Normalisation Practice | Independent Comparable Research | Integrated Valuation | Commercial Recommendation |

| Obtain the publicly available financial statements and management accounts for five small-to-medium businesses across different sectors; for each, construct the normalised EBITDA from scratch; document every adjustment and its rationale; compare your result with that of an experienced practitioner | For each of the five businesses, independently source comparable transactions or companies; document the specific comparability criteria; make adjustments for structural differences; derive a justified multiple range with a specific sector argument supporting the terminal value | Build a complete valuation for each business finance using the normalised earnings base and justified comparable range; present the output as a valuation range with specific assumptions identified; practise defending each assumption under active challenge | For each completed valuation, write a one-paragraph commercial recommendation: what does the valuation imply for the specific decision? What should the client do, and under what conditions? Get feedback from a practitioner on whether the recommendation is commercially credible. |

Real cases: the normalisation gap in professional practice

A mid-tier advisory firm’s graduate analyst was tasked with making an initial valuation of a professional services business finance acquisition candidate. She had done very well with her university valuation work in Australia and had no problem at all with the first six months of the job. She based her projections on the reported EBITDA in the financial statements when constructing the DCF. Her senior colleague checked the model and found that she had not been accounting for the founder’s remuneration at a rate above the replacement cost of management (which was $185,000), the cost of three years’ personal vehicles (which was a lot less than the market rate), or a lease at a related party rate that was significantly below the market rate. The unadjusted EBITDA was about 28 per cent higher than the normalised EBITDA. The valuation was founded on the unadjusted base, which significantly overvalued the business finance. In this instance, the problem was not the methodology, as the DCF structure was correct, but the normalisation step, because the university curriculum had never asked her to do this with real, imperfect financial data.

The second graduate had been normalising his own research on real management accounts for three months before his first advisory position. After 6 months in the job, he was handed the same assignment and completed the normalisation in about 2 hours, identifying the 3 material adjustments himself. His colleagues who had the same university preparation lacked this professional ability, as a result of the time spent on pre-employment normalisation practice. This is the outcome of deliberate and specific modelling practice, but not of generic modelling practice, Australian practical learning that lacks a focus on normalisation.

Conclusion

In the valuation context, there is no right or wrong way to do finance; it’s just a matter of what on-the-job training and formal education provide. There is a specific and measurable gap in finance education that can be filled with practice on real financial data – the five skill gaps listed above can be filled. The professionals who fill them before being put to the test in a professional role are in a materially better position than those who discover them under the pressure of a client.

For recent graduates, the biggest pre-employment or early-career investment is the ability to perform 3-5 normalisation exercises using real management accounts; it is the key skill that will underpin all other professional valuation skills and the most common skill gap in their early days in advisory practice.

Normalisation is the first step toward real-world valuation skills in professional practice; no amount of methodological sophistication compensates for the use of the wrong framework on the wrong earnings base.

To bridge the finance education gap, one has to practice with real-world, imperfect financial data—not pre-formulated exercises with complete information. The skills of making judgments in real valuation work in Australia only develop from exposure to the ambiguities that real financial data presents.

The gap refers to the difference between the theoretical knowledge taught in many university finance programmes and the practical skills employers expect graduates to demonstrate in the workplace. While universities provide strong foundations in finance concepts, employers often seek hands-on abilities such as financial modelling, valuation, data analysis, and business problem-solving.

Employers value candidates who can contribute immediately by analysing financial statements, building financial models, interpreting data, and supporting business decisions. Industry surveys show that practical experience and applied skills are increasingly important alongside academic qualifications.

Graduates may have limited exposure to practical skills such as financial modelling, business valuation, forecasting, investment analysis, Excel-based financial analysis, and real-world case study work. Employers are also placing greater emphasis on communication, teamwork, and commercial awareness.

Students can bridge the gap by participating in practical finance training, completing internships, working on real-world case studies, developing financial modelling skills, and gaining exposure to industry-standard tools and business scenarios. Combining academic learning with practical experience can significantly improve job readiness.

Candidates who combine theoretical knowledge with practical finance skills are often better positioned for roles in corporate finance, investment analysis, banking, valuation, and financial planning. Demonstrating job-ready capabilities can improve employability, accelerate career progression, and help graduates adapt more effectively to evolving industry demands.