Table of Contents

01

Introduction to the Skills Gap in Finance

04

How to Build the Gap-Closing Capabilities

02

What Corporate Finance Roles Develop — and What They Don’t

05

Real Cases and Lessons from the Field

03

Five Skills That PE Roles Require That Corporate Finance Doesn’t Develop

06

Conclusion

Introduction to the Skills Gap in Finance

The Skills Gap in Finance Between Corporate Finance and Private Equity

A common progression in the financial world in the Australian context is moving from corporate finance to private equity. One of the often-cited career advancement opportunities in the Australian financial landscape is the transition from corporate finance to private equity. The desire is valid: PE positions are in high demand, offer good pay, and are challenging in ways that suit the interests of many working in corporate finance. Much less frequently recognised is the nature of the skills deficiency of the two job types. The reason that some people can ladder faster into the finance world isn’t so much about the necessary academic qualifications or broad financial skills; it’s whether those skills have been explicitly developed in the corporate finance sphere.

One reason why skills for quick career transitions from corporate finance to PE are not generic corporate finance skills is that they’re specific to PE roles. In contrast, corporate finance roles just acquire them as a byproduct of their job. The FP&A professional who has worked in a corporate FP&A position for three years or more is well versed in Financial Management Reporting, Budgeting and Business Partnering Skills. They lack the skills to model LBOs, the investment thesis, and the commercial judgment to determine whether a business is an attractive LBO acquisition target at a given price. The gap should be specific, identifiable and addressable; and it must be specifically identified, not assumed, as part of general finance experience.

The article has been written for finance professionals looking to identify the specific capability gap between their current role and a PE role, and for those creating career-acceleration finance tips programmes who wish to help finance professionals close that gap intentionally. All five skill areas listed below are key areas where PE firms have identified gaps in their candidate populations when evaluating corporate finance analysts and associates.

What Corporate Finance Roles Develop — and What They Don’t

The genuine strengths of corporate finance backgrounds for high-performance finance professionals

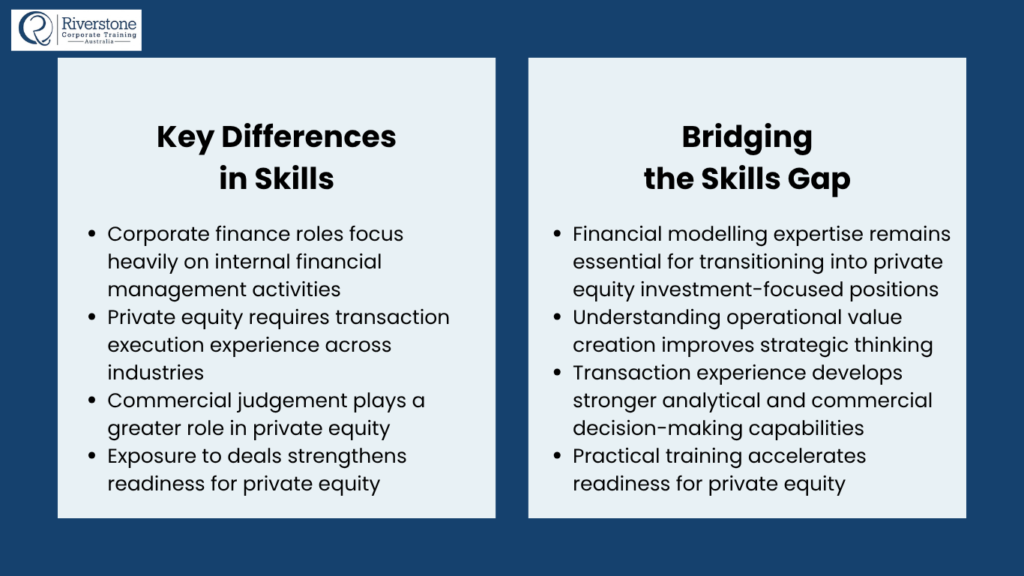

Corporate finance professionals with a proven track record of excellence in their jobs have essential expertise in the value that PE seeks: operating experience, quality of financial management reporting, discipline in budgeting, cash flow financial management, and collaborative work with operational management to enhance financial performance. These skills are actually very helpful in the post-acquisition value-creation process — the operational finance improvement that is often the biggest contributor to PE returns following an acquisition. Corporate finance professionals who know how to improve or worsen a business’s financial performance from the inside are not tripping over their own feet in PE.

• The operational and commercial judgment gained through a career in finance operating in a corporate environment is valued in the PE role, which focuses on post-acquisition operational improvement, but not necessarily in the pure advisory role.

• It isn’t a capability rebuild; it’s a capability gap-closing exercise. Building competitive advantage finance careers from corporate backgrounds requires an understanding of which corporate finance skills can be carried over and which need to be supplemented.

Where corporate finance roles consistently leave gaps for developing advanced finance skills

Three structural gaps need to be addressed to develop the more advanced finance skills required for PE from a corporate finance background. First up is the investment decision framework: corporate finance folks are trained to do financial plans; PE folks are trained to make investment decisions under conditions of uncertainty and to defend them. Second, the LBO modelling skill: corporate finance modelling emphasises operational performance; PE modelling emphasises acquisition structure, debt size, and equity return mechanics. Third, the market perspective: A corporate finance professional will know his or her business inside and out, while a PE professional needs to be able to make an instant judgment about any business in the sector, pinpoint the value drivers, and develop an opinion about whether or not the business is a good buy at the asking price.

Five Skills That PE Roles Require That Corporate Finance Doesn’t Develop

There are no random success factors in finance careers, whether in corporate finance or PE. Managers of corporate finance firms regularly look for five capabilities in candidates when evaluating for PE positions, and it’s best to directly address these capabilities in the job description to secure a competitive position.

| PE Skill Requirement | How Corporate Finance Leaves the Gap | Career Acceleration Finance Tips to Close It | Development Timeline |

| 1. LBO modelling from scratch without a template | Corporate finance modelling focuses on operational P&L, budgeting, and cash flow forecasting; LBO modelling requires understanding debt structures, return waterfalls, DSCR mechanics, and the specific relationship between entry multiple, exit multiple, leverage, and equity IRR | Build an LBO model from scratch for five different businesses using publicly available financial data; for each, vary the key inputs and practise articulating the IRR impact of each change verbally without referring to the model | 3–6 months of consistent practice; the LBO must be buildable from scratch in under two hours before any PE process interview |

| 2. Investment thesis construction and defence | Corporate finance professionals are trained to analyse financial performance and present findings; PE professionals are trained to form an investment thesis — a specific view on why a business is worth acquiring at a specific price — and defend it against active challenge | Develop two to three specific investment theses on real businesses in your target sectors: why this business, at what multiple, what is the value creation plan, what are the key risks, and what would make you wrong; practise defending each thesis against a practitioner’s challenge | 4–6 months; the thesis must be genuinely original and must survive the first follow-up question from an experienced practitioner without the defence collapsing |

| 3. Rapid business assessment from limited information | Corporate finance professionals know their own business deeply; PE professionals must assess an unfamiliar business quickly using an information memorandum or a financial model with limited prior knowledge of the sector | Practise the rapid business assessment: given a 20-page information memorandum, form a preliminary view in 90 minutes on the business’s quality, the key risks, and whether the indicative price implies an attractive return; practise doing this across five to ten businesses in different sectors | Ongoing practice; the ability to form a credible preliminary view in a limited time is what PE professionals are assessed on in early process meetings, and it requires sector breadth that takes time to build |

| 4. Sector knowledge at investment-decision depth | Corporate finance professionals understand their own sector from a financial management perspective; PE professionals need to understand their target sectors from an investment perspective: what drives the valuation multiples, what the key risk factors are, why recent M&A activity happened at the prices it did | Choose two to three sectors that align with your interests and the target fund’s coverage; read every major deal announcement, analyst report, and earnings call for six months; develop a specific view on the sector’s current valuation dynamics and what drives returns in that sector | 6 months of sustained engagement; genuine sector depth is identifiable within five minutes of a sector discussion with an experienced PE practitioner and cannot be fabricated |

| 5. Post-acquisition value creation planning | Corporate finance professionals understand how to improve a business’s financial performance from within; PE professionals must be able to develop a pre-acquisition plan for how they will create value after closing, including specific operational, strategic, and financial levers | For each investment thesis you develop, build a specific value creation plan: which three to five actions will you take in the first 100 days? What will drive EBITDA improvement? How will the exit multiple be earned? What does the returns model look like under the base, downside, and upside value creation scenarios? | Integrated with thesis development, the value creation plan is the commercial logic that justifies the price paid, and the returns model is the financial expression of that logic |

The gap that is most consistent between corporate finance professionals who have successfully made the transition into a PE career and those who are great at the technical mechanics of the investment thesis but lack in the commercial stage is skill in investment thesis construction and defence. Being able to analyse a business is not enough – you need to be able to develop and maintain a commercial view on whether the business is attractive to purchase for a specific pate; under what con,itions; and with what,lan of action to create value post acquisitionpost-acquisitionndly different way of thinking than that used in the financial performance analysis and operational finance work most corporate finance jobs demand, and it is honed through careful investment decision making, rather than further technical study.

How to Build the Gap-Closing Capabilities

A structured development pathway for the finance career growth strategies is needed.

There is a need for a structured programme spanning several months to address the five gaps listed above for a successful transition in career growth from corporate finance to PE. The four phases outlined below are the typical steps taken by corporate finance professionals who successfully transition to building capability.

| Phase 1(Months 1-3) | Phase 2(Months 2-5) | Phase 3(Month 4-6) | Phase 4(Month 5+) |

| LBO Technical Foundation | Sector Immersion and Thesis | Rapid Business Assessment | Process Practice |

| Build and stress-test LBO models for five businesses from publicly available financial data; practise returning IRR calculations verbally; understand the order-of-magnitude impact of each lever on the equity return; build speed until the model can be constructed in under two hours | Choose two to three target sectors; read every major deal announcement and analyst report consistently; develop two to three specific investment theses with full value creation plans; practise presenting and defending each thesis against active challenge | Practise assessing unfamiliar businesses from information memoranda in 90-minute sessions; form a preliminary investment view on quality, risks, and implied returns at the indicated price; do this for ten businesses across different sectors and document the view in each case | Run mock PE interviews with practitioners who will challenge the investment thesis, probe the LBO mechanics, and test the sector knowledge; debrief every session specifically; identify the gaps that emerge under pressure rather than in self-directed study |

Real cases: the transition that worked and the one that didn’t

When a corporate finance manager from a manufacturing company set his sights on a PE analyst position, he had 3 years of experience in FP&A and 1 year of commercial analysis. The other strategies he put forward in his application process were that his financial modelling was good but his LBO modelling was limited to a template he used in one of his previous positions; his investment thesis on the PE firm’s target industry was based on recent equity research, as opposed to independent research; he could not articulate a value-creation objective for any of the businesses he had discussed as a potential investment opportunity. He was turned down at the final round. Over the next eight months he worked specifically on each of the gaps: he built LBO models from scratch for twelve businesses, he gained and developed a genuine sector knowledge through regularly reading and attending one event a month from sector association and he created three fully developed investment theses to which he subjected himself to stress-testing by practitioner challenge. On his second attempt, he was offered a contract by a mid-market PE firm. It’s almost always a tale of focused preparation – not of overall financial prowess – for those who get into PE from a corporate finance track.

At the other end of the spectrum, a corporate finance professional has moved from a role within the PE fund to a role in its PE portfolio company. This journey allowed access to the investment thesis and value creation plan that had led to the PE firm’s initial acquisition decision, the post-acquisition operational improvement programme and the exit preparation programme. She was offered a position at the PE fund itself in two years of being on the portfolio company team, not as a typical analyst via the usual hiring process, but because the PE fund had seen first-hand what she could do at the company. Career acceleration finance tips: the PE portfolio company pathway is vastly underutilised by corporate finance professionals as a transition pathway; it builds the specific commercial and operational skills needed for the role in a PE fund, and it provides hands-on, real-world PE fund experience of the candidate’s quality.

Conclusion

Corporate finance does not naturally develop the five capabilities needed to grow into PE: LBO modelling, investment thesis construction, rapid business assessment, sector knowledge at investment depth, and post-investment planning for value creation. The finance career transition from corporate to PE isn’t a generic finance preparation problem: it’s a specific skill-building problem that requires targeted investments in the areas where there’s a gap.

Corporate finance professionals looking to join the PE arena: recognize that the basic level of finance skills is the ‘entry door’ for admission, rather than the differentiator and that the five areas above are the specific requirements and skills you need to focus on closing — and do so in a dedicated manner.

60% of the people who successfully moved from corporate finance into PE shared one characteristic: they deliberately spent 6 to 12 months preparing for the move and focused on the 5 skill gaps, not just on refining their corporate finance skills.

The company role is not being leveraged as a transition pathway; the PE portfolio company pathway allows for direct provision of investment and operational value creation at PE fund roles that demand it, and in an environment where the PE fund can first-hand witness the quality of the candidate’s work.

The skills gap in finance refers to the difference between the capabilities employers need and the skills many candidates currently possess. While academic qualifications remain important, employers increasingly seek professionals with practical experience, financial modelling expertise, data analysis capabilities, commercial awareness, and strong communication skills.

The finance profession is evolving rapidly due to technological advancements, data-driven decision-making, artificial intelligence, and changing business expectations. Many organisations report difficulty finding professionals who combine technical finance knowledge with practical business skills, creating challenges in recruitment and workforce development.

Employers frequently identify gaps in financial modelling, data analysis, forecasting, business partnering, communication, problem-solving, and technology-related skills. Recent industry research also highlights soft skills such as collaboration, presentation, and stakeholder management as critical areas where many new professionals require further development.

Finance professionals can strengthen their capabilities through practical training programmes, hands-on case studies, financial modelling exercises, industry certifications, and continuous professional development. Gaining experience with real-world business scenarios can help bridge the gap between theoretical knowledge and workplace expectations.

Professionals who combine technical expertise with practical business and communication skills are often more competitive in the job market. Closing skill gaps can improve employability, support career progression, enhance workplace performance, and prepare individuals for more strategic finance roles as industry demands continue to evolve.